.png)

You've found a strategy. The charts look clean, the logic makes sense, and you've watched the setups play out on paper. Now you want to put real money behind it, specifically, someone else's money through a prop firm. But between you and a funded account sits a challenge designed to weed out exactly the kind of unprepared trader who relies on gut feeling over tested process.

This is where backtesting becomes your single most important preparation tool. Not just to prove your strategy works, but to prove that you can execute it consistently, under pressure, with real drawdown consequences on the line. See how to pass a prop firm challenge using FX Replay as a starting point for your preparation.

This guide covers everything, from what backtesting actually is and why prop firms make it essential, to the exact process, metrics, tools, and mental frameworks used by traders who consistently pass challenges and grow funded accounts.

How to use this guide: Read it in order for a complete foundation, or jump to the section most relevant to where you are in your preparation. Each chapter builds on the last, but stands alone as a reference.

Before we get tactical, let's establish exactly what backtesting is, what it isn't, and why it's especially critical in the context of prop firm trading — where the rules are stricter and the stakes are higher than typical retail trading.

Backtesting is the process of evaluating a trading strategy against historical market data to assess how it would have performed in the past. The underlying assumption, and the reason traders trust it, is that if a strategy has a genuine statistical edge, it will show up repeatedly across different time periods and market conditions.

There are two primary forms relevant to manual prop traders:

You scroll through historical charts, identify qualifying setups based on your rules, and log them in a spreadsheet. Fast and accessible, but lacks realistic execution pressure, you always know what setup is coming next.

The market plays forward bar by bar in real time. You make decisions exactly as you would live without knowing what comes next. This is the gold standard for prop firm preparation because it replicates the psychological conditions of real trading.

A coded strategy runs across historical data automatically. This is for systematic/algorithmic traders. Most prop firm traders use manual or replay-based backtesting since their strategies involve discretionary decision-making.

Prop firm challenges aren't just profitability tests. They're behavioral stress tests. The daily drawdown limit, maximum drawdown cap, consistency rules, and minimum trading day requirements are all specifically engineered to identify whether a trader can perform under structured constraints, not just when conditions are perfect.

A trader who has backtested 200 trades knows their strategy's maximum consecutive loss streak. When that streak appears in a live challenge, they don't panic, they recognize it as normal distribution. That psychological composure is what separates funded traders from those who keep paying challenge fees.

The market doesn't know you're in a challenge. Your backtesting data should make you feel like it doesn't matter.

— FX Replay Community, Funded Traders Forum

Learn why most traders fail prop firm challenges and what the data reveals about the gap.

Most traders dive into backtesting without the necessary groundwork in place. This chapter covers the three critical foundations that determine whether your backtest produces useful data or just confirms your existing biases.

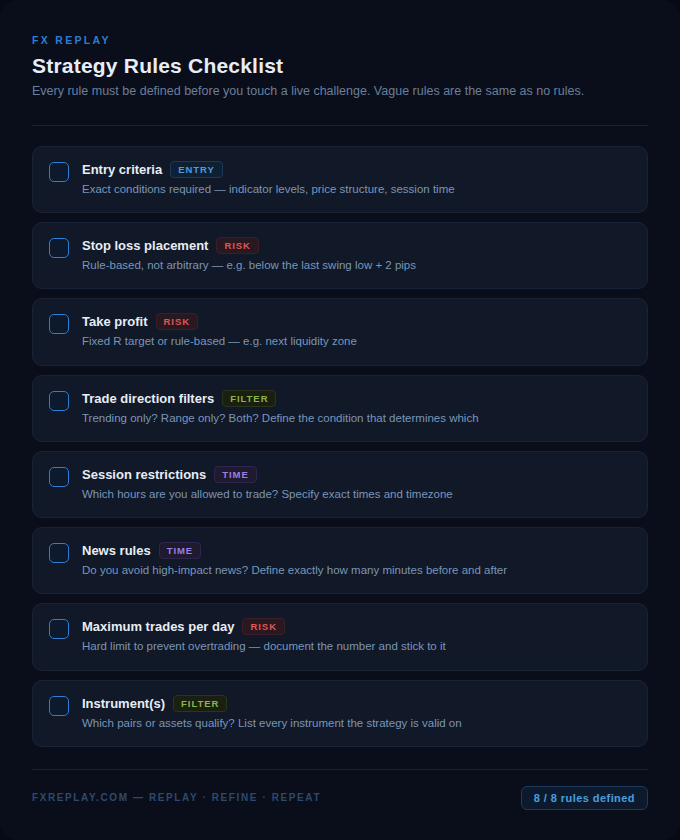

You cannot backtest a vague strategy. If your entry criteria is "price looks like it wants to go up near support," you don't have a strategy, you have an intuition. Before touching any replay tool, write your strategy rules in a form so explicit that another trader could follow them without asking you a single question.

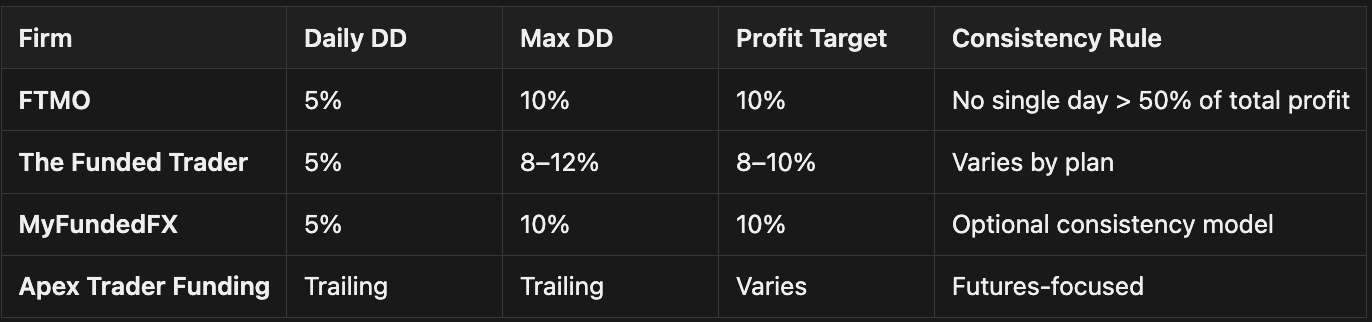

Different prop firms have materially different rules. FTMO's 5% daily / 10% max drawdown operates differently from a firm with a 4% daily / 8% max. Always backtest against the specific parameters of the firm you're targeting. A strategy that works comfortably inside one firm's rules may breach another's.

Your backtest is only as good as the data range it covers. Testing only on 2023 trending markets will give you strategies that fail in choppy 2024 conditions. Aim to test across at least 2–3 years of data, including volatile and ranging periods. FX Replay provides tick-accurate historical data across all major pairs going back multiple years.

💡 Pro Tip: Intentionally include a range-heavy period and a trend-heavy period in your backtest. If your strategy only shows edge in one condition type, you need to know that before taking a challenge.

Market replay backtesting simulates real decision-making pressure — the most realistic prop firm preparation available without paying challenge fees.

The backtesting process has five phases. Each phase feeds the next. Skipping any of them degrades the quality of your results and, more importantly, your real-world readiness.

Configure your backtesting tool to mirror your target prop firm's challenge parameters exactly. Set your starting balance, daily drawdown limit, maximum drawdown, and profit target. In FX Replay, these parameters can be entered directly so the platform enforces them during your replay sessions — just like a real challenge. Select your instrument(s), timeframe, and the historical period you'll test.

Run the market forward bar by bar. Apply your strategy rules as written. Place trades only when all entry criteria are met. Do not look ahead. Do not adjust rules mid-session. Log every trade — entries, exits, stop and target levels — and every no-trade decision (valid setup you passed on for rule-based reasons). Record your reasoning for each decision in your journal.

After the session, review each trade and tag it: A-grade (fully rule-compliant), B-grade (minor deviation), or C-grade (impulsive / emotional / off-rules). Calculate metrics separately for A-grade trades vs. all trades. The gap between those numbers is your execution deficit — the exact problem you need to fix before going live.

After 100+ trades, calculate all key metrics (detailed in Chapter 4). Look for weaknesses: Is the drawdown within the prop firm limits? Are there specific sessions or setups that underperform? Does the win rate degrade after a string of winners (overconfidence) or losers (revenge trading)? This analysis becomes your strategy's operating manual.

Based on your analysis, identify one specific area to improve, not a wholesale strategy overhaul, but a targeted rule adjustment. Retest with a fresh data sample. Repeat until your metrics consistently meet your prop firm targets across multiple testing periods. Only then should you move to a live challenge.

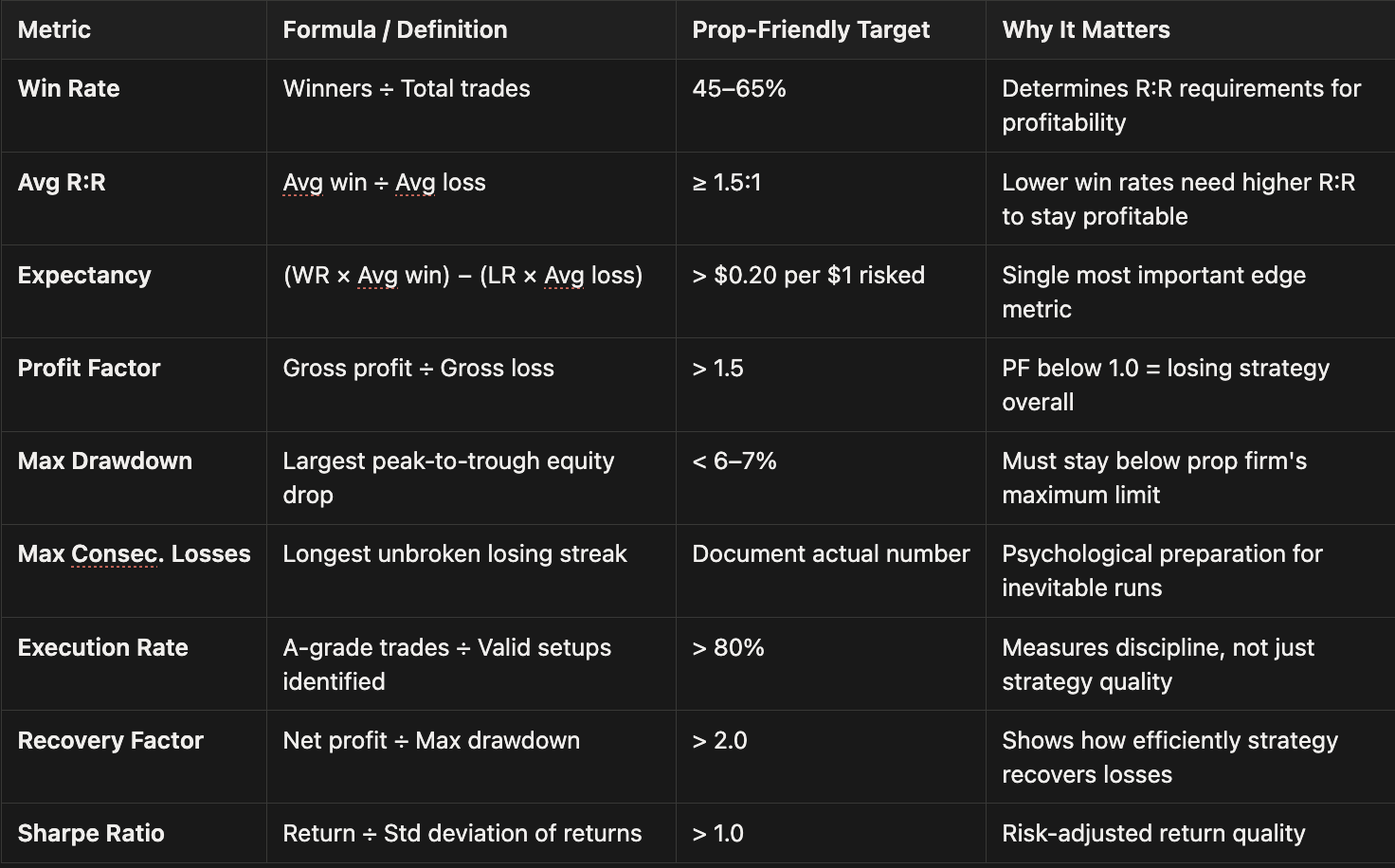

Backtesting without the right metrics is like training without measuring performance. These are the numbers that tell you whether your strategy is genuinely prop-firm ready, and which ones to trust most.

⚠️ Watch out for small sample sizes. A 20-trade backtest with 70% win rate means almost nothing statistically. You need at least 100 trades, ideally 200–300, before your metrics stabilize into reliable data. Prop firms will stress-test you far beyond any cherry-picked sample.

Your strategy's theoretical win rate is almost always higher than your actual win rate, because you don't execute every valid setup. FOMO causes late entries. Fear causes skipped trades. Overconfidence causes premature exits. Execution rate quantifies this gap, and improving it from 65% to 85% can have a larger impact on your challenge pass rate than any strategy optimization.

A proper market replay setup allows you to simulate weeks of challenge conditions in hours, training both strategy and execution simultaneously.

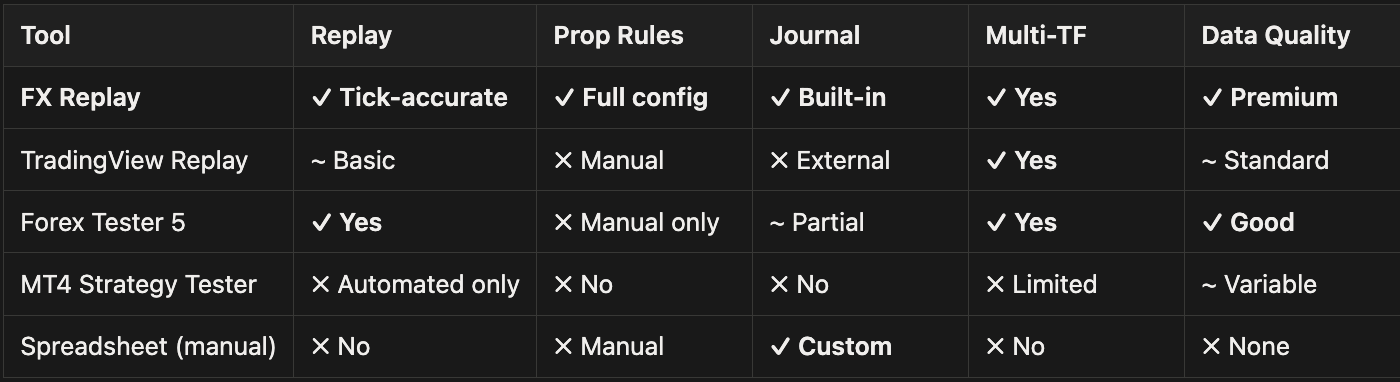

FX Replay is built specifically for the workflow described in this guide. The ability to configure prop firm parameters directly into your session — so the platform tracks and enforces your daily drawdown and max drawdown in real time, makes it uniquely suited for challenge preparation. Tick-accurate data ensures your results reflect what would have happened in real market conditions, not approximated bar data.

🔗 See also: How to Set Up Your First Market Replay Session in FX Replay, a step-by-step walkthrough for new users.

Adjusting your strategy rules during a backtest to improve the numbers you see, adding a filter that removes losing trades, tightening session times to avoid bad periods is curve-fitting. The strategy then only works on the data it was optimized against. In live trading (and in challenges), it will fail. Test your rules as written, always.

Skipping the replay forward to preview whether a setup plays out before placing the trade eliminates the only thing that makes replay valuable: uncertainty. If you know the outcome before you trade it, you're not backtesting you're confirming your existing opinions.

Testing only recent data (the last 6 months, the last bull run, the last trending phase) produces strategies optimized for a specific market regime. Prop firms don't pause challenges when conditions change. Extend your test window to cover at least 2 years and multiple market types.

A backtest that doesn't simulate emotional pressure is only half a backtest. Use replay rather than static charting. Set real challenge parameters so that a bad session creates genuine discomfort. The goal isn't just to test the strategy, it's to test yourself inside the strategy.

A single 100-trade sample is a starting point, not a conclusion. Forward test across a different time period. Test across a second instrument. Run the sample again 6 months later. A real edge shows up repeatedly.

Every time a valid setup appeared and you didn't take it and that's data. Were you afraid? Were you at your daily loss limit? Were you distracted? No-trade decisions reveal execution gaps that won/loss ratios never will.

Backtesting on clean mid-price data overstates performance. Always factor in realistic spread and especially for scalping strategies where spread represents a significant portion of the trade's value. FX Replay applies real bid/ask spread to replay data by default.

This is the chapter most backtesting guides skip. Strategy data matters but the way you use that data psychologically during a live challenge is what determines whether it helps you or becomes another source of doubt.

When you're on day 8 of a challenge and you've just taken 4 consecutive losses, your brain will tell you the strategy is broken. It isn't, you know from your backtest that your maximum consecutive loss streak is 6. That data is the anchor that keeps you from revenge trading, over-sizing, or quitting early.

The closer your backtesting environment mirrors the emotional conditions of a live challenge, the more your backtesting prepares you psychologically. This means:

Track your funded trader routine in FX Replay to build the discipline that challenges demand.

🧠 Elite trader practice: Set a consequence for breaking your rules in replay. Some traders require themselves to restart the entire backtest session if they break a key rule. The discomfort trains the discipline you'll need when real money is on the line.

Backtest data is reliable when it's based on 100+ trades, covers multiple market conditions, was executed with consistent rules, and includes a realistic spread. It becomes unreliable when sample sizes are small, data was cherry-picked, or rules were adjusted during the test. Know the difference before you put real challenge capital behind the numbers.

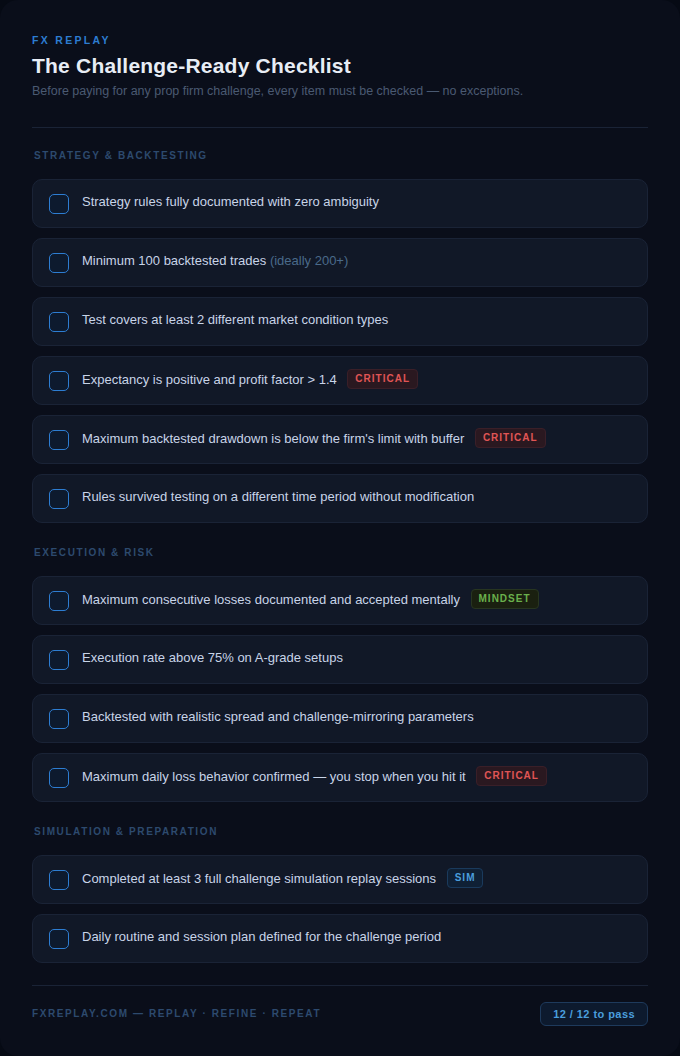

Before paying for any prop firm challenge, run through this checklist. Every item should be checked, no exceptions.

Log in to FX Replay and see if you can check off everything in the checklist now.

Couldn't find your question here?

Go check out our Help Center below!

Realistically, building a reliable 100–200 trade backtest sample takes 2–4 weeks of regular replay sessions if you're trading daily. Rushing this process and attempting a challenge on insufficient data is the most common reason traders fail repeatedly. Treat the backtesting phase as part of your challenge investment — not an optional step you skip to save time.

Yes. Liquidity, spread, and price behavior differ meaningfully between instruments. A strategy backtested on EUR/USD may behave differently on GBP/JPY. Always backtest on the exact instrument(s) you intend to trade in your challenge, and if you plan to trade multiple pairs, you need sufficient sample data for each.

Backtesting uses historical data to evaluate past performance. Forward testing (also called paper trading or demo trading) runs your strategy in current market conditions in real time. Forward testing is valuable for confirming backtesting results hold up in live conditions, but requires more time. Ideally, complete both before attempting a funded challenge.

This almost always points to an execution gap. In low-pressure backtesting, your discipline is high and your A-grade trade rate is strong. Under live challenge pressure, emotional trading takes over, you skip valid setups, take marginal entries, or exit trades early. Track your execution rate in your challenge journal and compare it to your backtest rate. That gap is the problem to solve.

Run a fresh backtest sample every 3–6 months, or whenever you notice your live results significantly diverging from your backtested metrics. Markets evolve, an edge that worked cleanly in one macro environment may need adjustment as conditions change. Regular retesting keeps your statistical edge current and your confidence in the strategy justified.

.png)