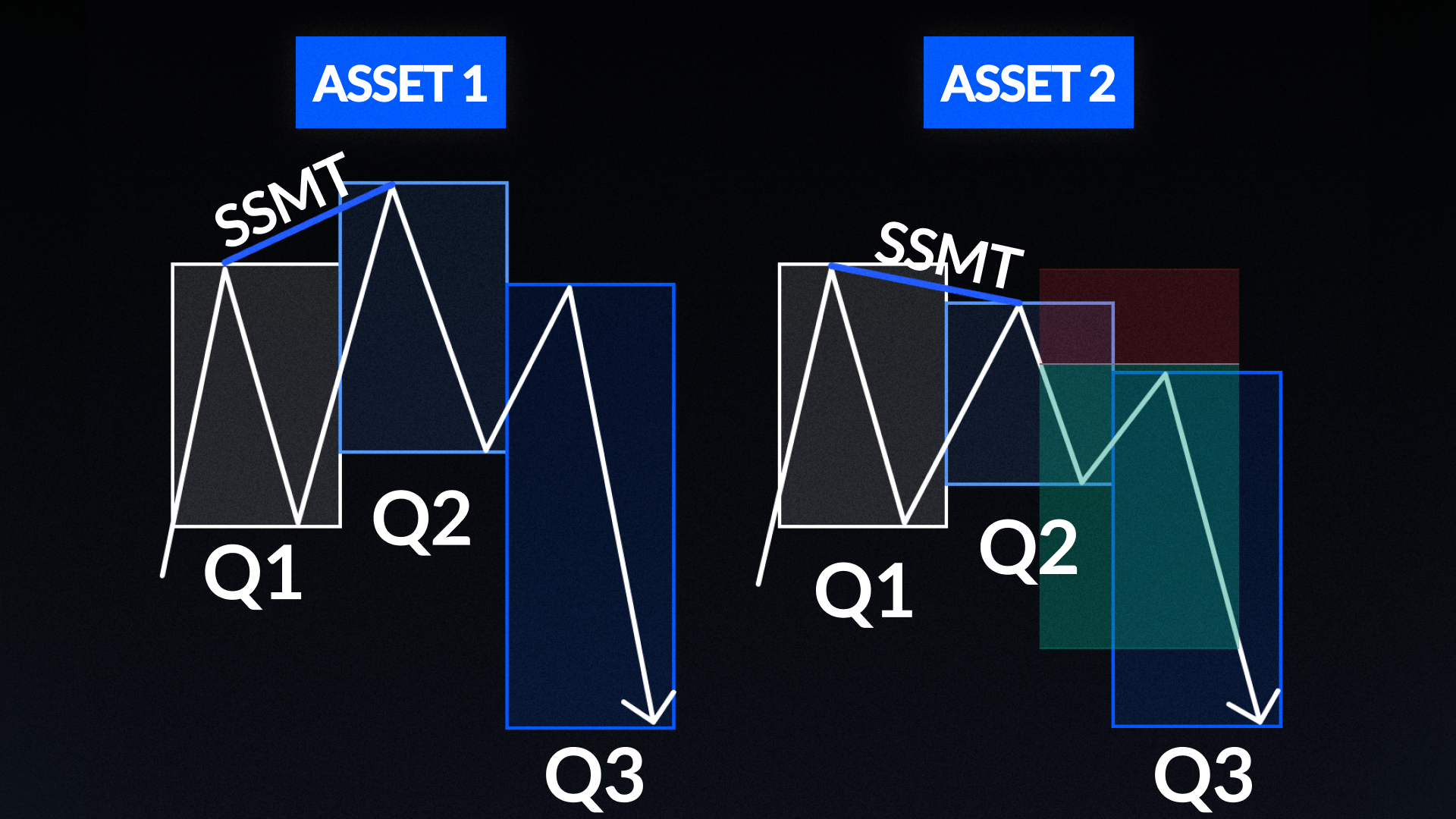

The Quarterly Theory SMT Strategy combines two powerful frameworks: Quarterly Theory, a time-based market cycle concept coined by Trader Daye, and SMT Divergence, the “crack in correlation” between two highly correlated assets. The core idea is that markets move in predictable four-part cycles across every timeframe, and when two correlated assets fail to confirm each other's high or low at a cycle boundary, it signals a high-probability reversal. The strategy is traded on the 5-minute chart using 90-minute quarters, primarily on EURUSD and GBPUSD during the London session, or ES/NQ during the New York session.

The specific variant used here is Sequential SMT, SSMT, a divergence that occurs between two consecutive 90-minute quarters rather than at a single point in time. When SSMT is identified, the trade is placed on the “highest probability pair”: the relatively stronger pair for longs and the relatively weaker pair for shorts. Entry is confirmed by either an engulfing candle or a Precision Swing Point, PSP, with a market order placed at that moment. The stop loss is set at the recent high or low that formed the SSMT, with a minimum floor of 5 pips, targeting 3R.

How the strategy works

Key concepts

Entry triggers

After SSMT is confirmed between two consecutive quarters, wait for one of two entry signals on the highest probability pair.

Trigger 1: Engulfing Candle

An engulfing candle forms on the highest probability pair after SSMT is identified. Place a market order at the close of the engulfing candle.

Trigger 2: Precision Swing Point

A PSP forms on the highest probability pair after SSMT is identified. Place a market order at the close of the PSP.

Trade checklist

- SSMT identified between two consecutive 90-minute quarters on two highly correlated assets, such as EURUSD / GBPUSD or ES / NQ.

- No invalidation conditions present, checked against the rules below before proceeding.

- Highest probability pair identified, stronger pair for longs and weaker pair for shorts.

- Entry confirmed by engulfing candle or PSP on the highest probability pair.

- Market order placed at close.

- Stop loss at recent high or low, or 5 pips minimum.

- Target 3R.

When not to trade

- Right before NY pre-market news, typically 8:30am NY time.

- When assets are moving out of tandem, with one trending up and the other trending down.

- When there is conflicting SSMT present before the entry signal.

- When there are relative equal highs or lows near your stop loss level.

No trade management once entered. Let the trade run to the stop or take profit. If any parameters are missing, trade quality is reduced. Aim to take only A+ setups.

.png)